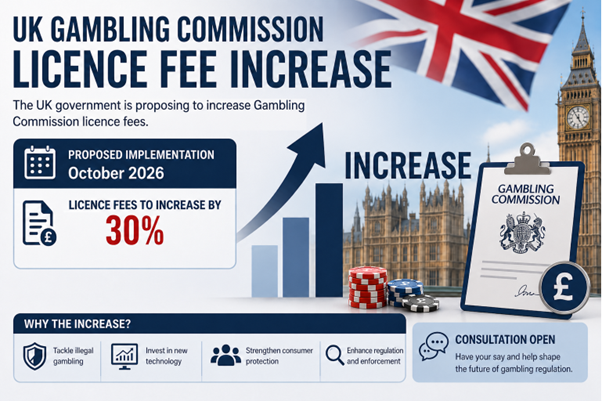

UK gambling licences are set to become more expensive both for registration and ongoing maintenance, with changes expected to take effect from 1 October 2026. This development comes shortly after major tax increases introduced in April 2026, creating a combined cost burden that could influence how operators structure high-cost verticals such as online casino and live dealer gaming.

The consultation proposes fee increases of 20% to 30%, with the government favouring a model that includes an additional portion specifically dedicated to tackling illegal gambling and protecting regulated market revenues.

Tax Increases

Taxation in the UK gambling sector has already increased significantly. The most notable change was the rise in Remote Gaming Duty, the tax applied to online casino and slot games, which increased from 21% to 40% in April 2026. A new unified betting duty is also expected to apply from April 2027, further adding to the financial pressure on operators.

Large multinational companies are generally better positioned to absorb these increases. They operate across multiple markets, have larger balance sheets, and can spread compliance costs across a broader revenue base. Smaller and mid-tier operators, particularly those focused primarily on the UK, may not have the same flexibility. Those heavily reliant on casino revenue are likely to feel the pressure most, as casino products tend to carry higher tax rates and operating costs.

In response, some businesses may look for ways to reduce expenses, including cutting marketing budgets, streamlining staffing, or reconsidering where they locate parts of their operations. Regulatory costs have historically influenced where gambling companies choose to operate.

Further Market Differentiation

Back in 2023, parts of the iGaming industry advocated for a single unified tax covering all online gambling products. The government ultimately chose not to adopt that approach.

Instead, the current framework continues to differentiate between products based on perceived risk and social impact. Instant games such as slots and online casino products are widely viewed by policymakers as carrying higher levels of risk, and they are therefore taxed more heavily. Betting products generally face lower rates, while retail betting and horse racing often benefit from more favourable treatment due to their economic and cultural ties to sport.

This spread of taxes can make some popular iGaming verticals, such as live casino UK offerings, less available, even though there’s a strong demand for them among players.

New Compliance Demands

Beyond fees and taxes, operators are also facing a growing list of compliance requirements. These include more detailed reporting obligations, enhanced affordability checks, and stronger consumer protection measures.

For some companies, that may mean hiring additional personnel rather than reducing headcount. In other cases, businesses may attempt to offset those costs through automation or process improvements.

Regulatory Funding and Policy Context

Financial pressure on the regulator has been building for several years. The Gambling Commission used £3.1 million from its reserves in 2024–2025 and expects to draw down a further £5 million in 2025–2026, with projections showing reserves could be fully depleted during the 2026–2027 financial year without a fee increase. Without additional funding, the Commission could struggle to maintain enforcement capacity.

More resources are expected to be directed toward tackling unregulated operators, developing new monitoring technology, and implementing reforms introduced following the Gambling Act review. In that sense, the fee increase is less about generating revenue and more about ensuring the regulator can keep pace with the scale and complexity of the modern gambling market.

Some industry observers believe that once major technology investments are completed, regulatory costs could stabilise. However, there is currently no clear indication that taxes or fees will be reduced in the future.

Changing Operator Strategies

Rising costs rarely leave business models unchanged. As fees and taxes increase, operators are likely to look more closely at efficiency and profitability. That could mean fewer promotional offers, tighter control over marketing spending, and a stronger focus on products that deliver more predictable returns.

High-cost verticals require significant spending on technology, licensing, and content, and those investments become harder to justify when margins are squeezed.

In some cases, operators may also consider basing parts of their operations outside the UK. A recent example is Sky Bet, which relocated key operations to Malta in 2025, a move widely reported as a cost-saving measure that could reduce its tax burden by as much as £55 million annually.

Operators will also need to balance cost control with regulatory expectations, as new compliance requirements often require additional staff in areas such as responsible gambling and financial monitoring.

Competitiveness Concerns

One of the recurring themes in industry discussions is competitiveness. The UK remains one of the largest and most trusted regulated gambling markets in the world, but it is also becoming more expensive to operate in. As costs rise, the relative attractiveness of other jurisdictions becomes more relevant, particularly for smaller operators.

Smaller operators are particularly sensitive to these changes. Unlike multinational firms, they may depend heavily on a single market and have limited capacity to absorb unexpected costs. For those businesses, even modest increases in licensing fees or taxes can have a disproportionate impact.

In extreme cases, companies may decide to exit the market or shift their focus elsewhere. More commonly, they may simply slow investment, delay expansion, or reduce hiring.

The Risk of Unregulated Market Growth

Another concern raised by analysts is the potential growth of unregulated gambling activity. When legal markets become more expensive to operate in, the risk is that some consumers and operators may look for alternatives outside the regulated system.

iGaming industry commentator Andrew Lamb has suggested that excessive regulatory pressure could reduce participation in licensed markets, potentially increasing the share of gambling taking place outside regulated channels. If that happens, governments could see lower tax collection while consumers lose the protections that regulated operators are required to provide.

The policymakers emphasize they would use the increased funding to combat this phenomenon; roughly £2.6 million per year would be ringfenced specifically for tackling illegal gambling and protecting licensed market revenues.

Comparison with Other Markets

International comparisons highlight how widely regulatory costs can vary. Some jurisdictions, such as Malta, are often seen as relatively cost-efficient, with predictable licensing structures and lower operating expenses. For example, Malta licence application fees can be as low as around €5,000, with annual fixed fees starting at roughly €25,000, making it one of the more accessible regulated markets in Europe.

Others, including markets like Italy, can involve significantly higher upfront costs and more complex regulatory requirements. Under the country’s latest reform, a single online gambling licence now costs €7 million for a nine-year concession, compared with just €200,000 in the previous licensing round. Operators must also pay annual charges of around 3% of gaming revenue, along with additional financial guarantees and compliance requirements.

The UK sits somewhere in the middle. Depending on the licence type and revenue band, maximum annual licence fees can reach roughly £790,000, while application costs can exceed £90,000 for the largest operators. These figures are significantly higher than those of smaller jurisdictions but still far below the entry costs seen in markets like Italy.

What sets the UK apart is scale. The country remains one of the largest regulated online gambling markets in the world, and that size has historically supported strong participation from both operators and players.

The question now is whether the combination of higher taxes, rising licence fees, and expanding compliance obligations will gradually change that balance.